| 2013-10-31 |

US markets continue to be dominated by the on-going corn harvest and the likelihood of a record crop which is seen weighing on wheat values.

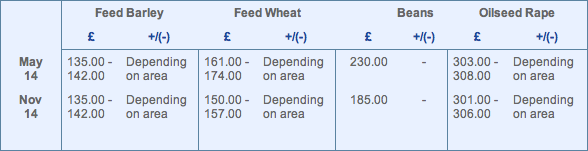

Feed Wheat

With the US wheat market down $9 on the week (firmer US$ and un-winding of corn/wheat spread) the MATIF is down €2 and LIFFE is unchanged. US markets continue to be dominated by the on-going corn harvest and the likelihood of a record crop which is seen weighing on wheat values, especially with US winter wheat plantings on average pace (86% complete) and weather/ crop conditions both reported at favourable.

EU values, slightly supported by a weaker currency has seen only limited movement, as traders still point to hopes for more export interest in EU wheat. Southern hemisphere concerns, Black sea quality issues and Australian/Canadian logistical issues all have EU traders believing export demand, especially for French wheat will increase over the next few months .However with the size of the French crop – export demand is definitely needed .

UK values, mainly driven by spot demand into the North remain underpinned. The recent return of more adverse weather conditions has slowed sowings for the 2014 harvest, and although the planting window is still open, the final planted wheat area may struggle to reach the 2mln+ hectares being projected by analysts , although this figure remains achievable .

In summary, markets have reached a cross-road in determining future price direction. The record US corn harvest will ensure that for the second half of the season there will be more than ample supplies of coarse grains across the globe. Wheat demand (shipments) are running well ahead of forecast from all the major exporters (US/EU/FSU) but with the onslaught of cheaper corn, this may well dampen importers enthusiasm to extend wheat coverage. Despite earlier concerns Black sea sowings have ‘picked-up’ the pace over the past 10-14 days, and final area losses are likely to be less than first feared. Spot sentiment remains supported but that could be the best reason to sell .

Oilseed Rape

It’s been a fairly slow week on oilseeds with the market waiting for the USDA report and export numbers. The market is anticipating large export numbers for soybeans and a yield and production increase, we also have question marks over the planted and harvested acreage figure for US soybeans. The US harvest is now around 80% complete.

In South America improved plantings continue and we have seen better conditions in South America.

In Europe trade remains slow, crush margins are attractive and we have strong meal demand but we don’t see huge volumes of farmer selling. The matif rapeseed contract is trading in a range with little new input. UK domestic prices eased earlier in the week in line with matif but they were supported by the strength of the Euro versus Sterling.

Oats

The market remains under pressure at the quality end of the market as millers move their delivery requirements towards Feb/March.

There is more demand within the feed sector as borderline milling parcels look attractively priced to the compounder.

The continued lack of exports continues to give the oat miller the controlling card in this market.

Malting and Feed Barley

This week has seen some large tonnages enter the market as sellers come forward both off farm and in the trade.

There remains to be little domestic demand into malting homes pre-Christmas with no sign of any large scale post-Christmas demand in the short term.

FOB markets remain quiet as EU buyers are looking to cover their 2014 harvest demand with guaranteed old crop quality that they will carry over from this season’s large good quality crop.

There are still markets available and Gleadell advise growers to be selling their old crop tonnage as become available.

Gleadell still have contracts available for 2014 crop with limited tonnage left in the pre-Christmas positions including harvest movement. These include contracts for distilling and winter varieties.

The availability of low risk contract options paired with a 1.92 nitrogen spec for domestic markets sees Null-lox as a good choice for Spring barley growers.

Seed

Spot demand remains for winter wheat and barley. This looks set to continue towards the end of the year, particularly on land behind root crops.

We have late drilling options including Conqueror, and other varieties including KWS Kielder/Cougar/Icebreaker and Invicta.

The best Barley option remains SY Venture, with the potential of malting premiums .

Turning the focus to the spring, the late autumn/spring drilled wheat option Mulika is set to be in strong demand, with the option of drilling November/December and then into the spring if the weather closes in. Mulika has the added benefit of being a quality wheat for which attractive premiums are available, and new spring quality wheat Dafne is also available, yielding similarly to Mulika once again with excellent quality.

Gleadell still have demand on the Null-Lox barley contracts, and the varieties which remain available are Cheerio/Cha Cha and the new variety Chapeau.

Peas are also in the spotlight for this coming spring. Many growers have had a really good year and for many their pea crops will return the highest gross margin crop on the farm, and certainly help as part of a balanced rotation.

The marrowfat variety Kabuki and large blue Daytona are available with very attractive buyback contracts.

Mainstream barley varieties are also now available. Varieties Odyssey/Concerto/Sanette and Propino which have all had good years will be in demand.

Spring Oats and spring beans may also be on some people’s radars. Spring bean seed is currently trading at the same price levels as winter beans where more normally you would expect to see a £100/mt premium – so it could be a good time to lock in your requirements. Gleadell can offer Fanfare, Fuego and Pyramid and the Spring oats Canyon and Firth.

Fertiliser

Ammonium Nitrate

Acceptance of amended values has resulted in strong uptake of GrowHow Nitram for the November to January delivery period. With AN values equating to around £40 - £55 per acre for arable growers, against current forward values for wheat and oilseed rape, the opportunity to lock in margin is definitely there.

Potash

Internationally confidence is starting to grow in potash values, with UK values still trailing along the bottom. The Russian potash saga has disappeared from the news, with back ground peace making and deals going on. Brazil is a buyer of Russian and UK potash, at values equating to £270/t delivered farm bagged, a value we are currently trading below.

Phosphate

Improved trading conditions and post monsoon demand in India is seeing a vacuum for product appear. Product from as far North as America has been sold into India. On a UK basis, there has been little change, values will get dragged by world demand, as North African and Russian producers will all be looking at homes further afield.

Urea

India is set to tender for around 2 million tonnes of urea. This coupled with short covering of sales into Europe is driving price expectations up for Egyptian producers. North African values have firmed by $10/t in the past week, equating to £7/t rise in UK farm values. Current stock positions are giving growers some discount to full replacement value, but will only be sold off once.

SKW Piesterit

We are suppliers of quality German manufactured products from SKW Piesteritz. Piamon and Alzon 46 are currently available, providing UK growers with an alternative and proven European fertiliser system.