| 2015-08-13 |

Already feeling the backdraft from the Chinese currency devaluation, commodities were dealt another hammer-blow as the USDA produced a report which took the market by surprise.

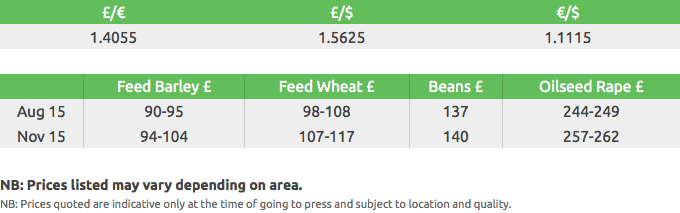

Feed Wheat

Whilst US wheat production was trimmed slightly, it was the scale of increase in US corn / soy yields, production and ending stocks that produced the sell-off after the report was released. US crop ratings are no better than they were at the beginning of July, so does this merit the increase? The trade thought not, USDA did, and that is what apparently counts in the long run! Wheat markets continue to be following rather than leading – export inspections are running 23% behind last season’s pace, so wheat still remains heavily over-priced and with little fundamental support.

The EU market, while showing some support recently on concerns relating to the diminishing EU corn crop, followed Chicago lower. News that the second MATIF futures store (Rouen) has suspended intake did little to relieve harvest pressure. Increased production for the Black Sea region, of 5mln mt, will not only keep EU values honest, but increase the importance of getting the Russian tax situation resolved as soon as possible, as the 22% slip in the ruble since mid-May is hurting exports, but supporting interior farm levels.

The UK is still operating under the spot market regime. Prices have fallen as reports of large yields place additional supplies into a market already awash with abundant old crop supplies and limited demand. As the harvest moves north and west, premiums in these areas have diminished, with the market in the south and east now trading at a larger-than normal discount in order to secure movement.

In summary, the last week has been a bull’s worst nightmare! Firstly concerns over China and lowering demand, followed by a bearish USDA report. The corn / soy numbers released virtually eliminated any risks to the supply side, which was seen as supporting the recent spike, especially within the corn market. For wheat, nothing much has changed – US fundamentals look bleak, and whilst corn held a glimmer of light, that has now been extinguished – meaning unless there is a total southern hemisphere disaster, wheat markets will struggle to hold onto any rallies.

Malting Barley

EU malting barley prices are under pressure from the fundamentals of another large barley crop this year as yields continue to exceed expectations.

Yields of winter barley in the UK are up 15% from last year and early reports from the spring barley cuts suggest above average yields and reasonably good quality, this is adding to an already larger planted area compared to 2014/15.

Harvest in Scotland is approximately two weeks behind and there is uncertainty surrounding the quality of the barley crop after poor weather hampered growing conditions; the situation is similar in Scandinavia.

Malting barley prices are tracking those of the wider feed grain market and premiums have tightened.

Buying interest for malting barley across the EU is limited and UK FOB values are weaker as a result.

Few markets are appearing as buyers look to cover shorts and although free market harvest movement is very limited, there are markets for later in the season.

Feed Barley

The UK feed barley market continues to be dominated by movement opportunity.

The break in sterling strength earlier this week did little to encourage barley exports as a lack of bids remains the issue in the nearby positions.

Large yield reports continue as reflected by last week’s ADAS report, which raised its winter yield figure to 7.2t/ha.

There has been little change to the domestic picture. Consumers remain steadfast in their decision to wait for lower prices unless the purchase is against feed sales.

UK barley is still uncompetitive for ‘big port’ export business in the deferred positions.

Rapeseed

A crazy half an hour last night followed the USDA report. USDA came out with some very unexpected higher yield numbers taking traders and analysts by surprise. The trade was anticipating a cut in yield so the increase in production wrong footed the market, volatility went crazy as funds dumped millions of tons of beans, CBOT soybeans were down around 60 cents or circa 6% in a matter of minutes.

MATIF rapeseed followed beans lower, down around €9 on the day. Short-term direction is now hard to call with volatility high. Longer-term, rapeseed fundamentals remain mildly supportive with a lower global crop figure, but at present soybean volatility could dictate market direction.

Oats

The winter oats Mascani and Dalguise continue to give good quality results and yields above average but not as spectacular as some of the wheats.

There is not undue harvest pressure for movement as growers wait for another day. This is perhaps partly explained by the DEFRA figures released today of a 6.5% drop in plantings in England.

Spring oats to date are nearer 52 kg.

Winter oats are starting to be cut in the Borders and we await information from this region.

Milling Wheat

UK milling wheat premiums continue to come under pressure in the short term, with limited miller demand still offering very little support.

Despite sterling weakening versus the euro since last week we have seen the differential between UK and German A (13%) values narrow, again limiting the upside for UK premiums.

Export potential for Algeria business remains unlikely for now, with French wheat offered considerably cheaper.

With circa 35-40% of the UK’s milling wheat cut quality appears to be generally very good, although with variable proteins. Average proteins for Group 1 varieties, at this stage, are 0.5% higher than the 14/15 season.

Pulses

The value of beans remains linked to LIFFE wheat futures. We have seen significant interest from feed compounders this week who are now keen to use beans at these values. The human consumption market remains very difficult .The restrictions on accessing hard currency in Egypt continue to prevent buyers coming to the market. Whilst many of the buyers are keen to buy, there are concerns about their ability to access US dollars to pay for the goods. This in turn results in very few offers from exporters. If and when these restrictions are eased is anybody’s guess.

The pea harvest is now well under way with yields reported to be above average and the samples we have seen have all been very good quality. Based on the high yields we have been hearing we expect the market to come under significant pressure in the coming weeks.

Seed

Gleadell is in an excellent position to be able to offer quick delivery across a number of key oilseed rape varieties. Gleadell’s oilseed rape portfolio offers growers a range of varieties, many of which have performed extremely well in this year’s trial results.

For conventional growers looking for a variety with the best all round performance Campus is one to look out for. “The seed with speed” has rapid autumn development, high yield potential, excellent oil content and solid agronomics.

Incentive has remained a consistent performer again this

year, keeping the confidence of growers. Its seed yield and oil content both

combine to produce a high yield potential.

Wembley is the top hybrid candidate on the 15/16 Recommended List for the E/W region. Wembley has shown a good performance in trials and looks set to be a solid all-rounder.

Another new hybrid candidate variety which has been performing exceptionally well in trials with consistent results is Windozz from breeder RAGT. Windozz combines good early vigour, early flowering, early harvest and a high gross output.

Fertiliser

Ammonium Nitrate

European markets remain quiet as harvest continues. With shipments from

the Achema factory now moved to September, Imported values have remained

stable for both August and September delivery periods.

GrowHow has held terms at current levels, so prices remain at a £10/t premium to imported product. However, values are likely to increase by a further £3/t for September and monthly thereafter.

Urea

Globally, prices look to have stabilised as US markets continue to firm steadily for nearby months and Q4/1.

UK importers have moved prices up to reflect this move.

The global supply outlook remains short so further price increases are expected.

P&K

Straight phosphate and potash levels are still trading below replacement in the UK, with blends trading at further discounts to encourage buyers.

However, blenders need to increase levels as many are operating well below the cost of production so we would expect price rises on PK fertilisers next week.

We urge any buyers of PK to take advantage of lower levels and purchase now.

Alzon 46

Alzon 46, produced by SKW Piesteritz, guarantees constant high quality and is exclusive to Gleadell in the UK.

Stabilisation of the nitrogen results in significant benefits, such as higher efficiency, fewer fertiliser applications, improved plant nutrition and, not least, environmentally friendly fertilisation.

The stabiliser controls the release of nitrogen up to 14 weeks, from stable ammonium to mobile nitrate, achieving a balanced nitrogen supply in line with crop demand.

Fibrophos – why pay more for your PK fertiliser?

The complete base fertiliser, containing all the nutrients (less nitrogen)

a crop requires to grow.

Spread onto stubbles, Fibrophos replaces the range of secondary and trace elements in a ratio similar to that removed by the previous crop.

Be entered into the draw to win a full load of Fibrophos or P-Grow worth £3000 by placing this seasons requirements with Gleadell.

To find out more speak to your Gleadell Farm Trader or Fertiliser Department on 01427 421 244.