| 2015-07-10 |

After last week’s sharp upward movement, wheat prices have eased back on more favourable weather outlooks for key producing areas.

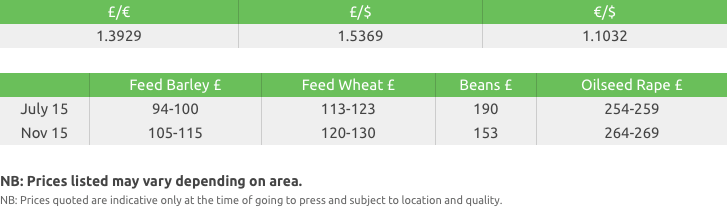

Feed Wheat

US winter wheat harvest is now over 50% complete, and although wheat crop ratings slipped on the week, they still remain ahead/in line with last year. Funds have now switched from their record short position into being long on recent weather scares, leaving the market more vulnerable on the downside if conditions improve.

EU markets have also retraced from recent highs, following US markets lower. The heat that threatened crops across much of mainland Europe is slowly diminishing, although additional rainfall is needed in certain areas. Crop damage due to the heat seems to have been limited, confirmed by the recent crop estimate by the French agriculture ministry that places the country’s soft wheat crop at 37.9mln t, up 1% year on year. Black Sea values are slightly firmer, although confusion on the export duty (as based on US fob levels) is evident on export quotes.

The UK market has moved lower, pressured by the reverse in global direction and the un-competitiveness of UK supplies. While the recent rise encouraged some producer selling, domestic buyers were less enthusiastic about following the market higher. The AHDB Cereals and Oilseeds Planting and Variety Survey released this week shows the GB wheat area for the 2015/16 crop at 1.87mln hectares, down 3% from 2014. Working on average yields the UK should produce a crop of circa 15mln t, down from this season’s 16.6mln t.

In summary, last week prices seemed to be heading into the stratosphere, so what has changed? The weather outlook has improved, US crop ratings are stable and funds are now long. One of the key bullish factors, concern over the US crop, has been removed, leaving weather the main support. As conditions seem to be improving and harvests progress, market fundamentals should start to gain hold of the market, which currently for wheat, and especially US wheat, remain far from bullish on their own.

Milling Wheat

The French wheat harvest has continued to progress well, with the heat of the past few weeks appearing not to have caused overly significant crop losses.

Good quality continues to be reported, allowing for French wheat to be first-in-line for Algerian (11.5% protein) business.

Last week’s 400,000t new-crop Algeria tender saw UK values some £8/t too expensive to compete.

With currency remaining volatile, especially due to the uncertainty surrounding Greece, this margin could widen or narrow very quickly.

Our domestic milling wheat situation remains very much the same as last week with weak miller and flour demand causing premiums to trickle lower.

UK premiums over feed are currently settled just below the 5-year average, at circa £22-£23/t.

With slightly lower UK premiums, the premium for German imported milling wheat (13% protein) over UK values has widened.

The AHDB’s planting survey pegs combined UK Group 1 and Group 2 plantings for 2015 harvest at 23%. With notable increases for Gp1 varieties the main focus must now be on the weather over the coming weeks.

The crop must avoid much cooler temperatures or heavy rains towards the end of its growth, however so far conditions in the UK have been favourable.

Malting Barley

The weather in France has sustained concerns over the condition of spring crops however, the forecast shows temperatures are likely to ease over the coming week.

Australia is experiencing low temperatures and low levels of precipitation.

Buying interest is minimal for both crop years as we await harvest with little fresh news helping to find a new price direction.

Intake for distilling malting barley varieties in the UK has been pegged lower over the coming seasons following a contraction of the UK distilling market and the fact maltsters have benefitted from big carryover stocks.

There have been good results from the French winter barley harvest showing above average yields and good quality in many regions.

Malting premiums are strong, supported by the aforementioned weather concerns, and the number of sellers has picked up as growers take advantage of the current premiums on offer.

Rapeseed

Rapeseed futures markets have been very volatile over the week with intraday swings of up to €8. The market has pulled back on profit taking and the slowly progressing harvest. Real harvest pressure hasn’t been felt yet with limited selling across the continent. Rapeseed fundamentals have a bullish bias this year but the harvest period could see some pressure.

The ongoing situation in Greece continues to create uncertainty regarding the euro, adding volatility to UK rapeseed prices.

The US soybean market also remains volatile as we have seen heavy fund position covering on weather/planting concerns.

Oats

The AHDB oat planting survey released on July 6 indicated that GB plantings were up one percent. If this proves to be correct and yield returns to trend we have a tighter balance sheet especially as the old crop carry in appears to be back in line.

Winter oats in the south are ripening at speed and first fields could be seen week commencing July 20.

Pulses

We have received a few enquiries from Egypt regarding new crop human consumption beans this week. However, the buyers continue to have difficulty obtaining access to hard currency and we do not expect the situation to improve any time soon. We have also heard reports that buyers in Egypt are intending to source beans from non-traditional origins which will increase competition into this market.

We have some limited availability for the 16/17 Kabuki pool in the Jan/Mar position. Please contact your Farm Trader for more information.

Seed

There has been an increase in demand for winter wheat seed this week as growers are making their cropping decisions.

This week has been another busy week on seed, with rallying markets growers have been looking to fix prices due to the current volatility.

KWS Lili is top of the Group 2s having a UK yield of 105, equal to the likes of KWS Santiago and Leeds. Part of KWS’ “Dynamic wheats” portfolio, it offers grain quality and high yield, giving growers more market options.

Syngenta’s new variety Reflection is the highest yielding variety on the Recommended List. This new addition offers growers an excellent combination of disease resistance, untreated yield and robust agronomics as well as earlier maturity than its competitors, allowing growers to spread their workload.

Hybrid barley ’s vigorous early root growth and extremely high yields could, according to reports, reduce blackgrass return by 91% due to its competitive growth and canopy. Volume is the highest yielding hybrid on the Recommended List and Bazooka is the highest yielding candidate variety, both varieties are part of Syngenta’s “Cashback Yield Guarantee.”

Wembley, from Limagrain, is top of the candidate region for the East/West Region. It has high lodging resistance, good disease scores and an oil content similar to Incentive.

Campus is the best all round conventional oilseed rape variety on the new RL and was the top conventional in 2014 in both East/West and North regions, making it an excellent choice for growers in all areas. Its rapid autumn development, stem stiffness and disease resistance makes Campus a solid variety.

Fertiliser

Urea

Global markets have slowed this week on the back of easing demand in the west. Demand in the US and Europe is expected to be seasonally slow until August/September.

The next significant demand is expected to be from a new Indian tender in August and is likely to indicate the next move in the market.

In the UK, offers remain £20-30/t below replacement values and means that any global price moves are unlikely to significantly alter UK levels at present.

Alzon 46

Exclusive to Gleadell Agriculture in the UK, Alzon 46 is produced by SKW Piesteritz, the largest urea producer in Germany.

Alzon 46 is a granular 46%N urea with an incorporated nitrification stabiliser which enables a slow release of nitrogen up to 15 weeks depending on weather.

The benefit is that larger doses can be applied reducing passes by one and reducing the risk of losses and luxury uptake.

Ammonium nitrate

The end of last week saw the news that Yara International had agreed to sell their 50% shareholding in GrowHow UK Group Limited to CF Industries. Once the deal is concluded GrowHow will be a wholly owned subsidiary of CF.

The UK market has seen slower demand over the past week as a significant amount of growers booked at least some of their requirements when new season prices were announced.

With a large tonnage already booked we expect GrowHow to stick to its stepped price increase plan over the coming months.

Buying at current prices could be a better decision than delaying purchasing.

Imported product continues to trade at roughly a £10/t discount to UK product. We expect price increases similar to UK levels.

P and K

The global phosphate market remains firm with high demand from key importing nations. Potash continues to trade sideways.

In the UK, demand and price for PKs and NPKs remains steady. However, as growers start ordering for the autumn, prices might rise to reflect higher replacement values.