| 2015-03-20 |

One of the most critical period for the market begins in the weeks ahead, as farmers, especially in the US, plant spring crops and winter crops emerge from dormancy.

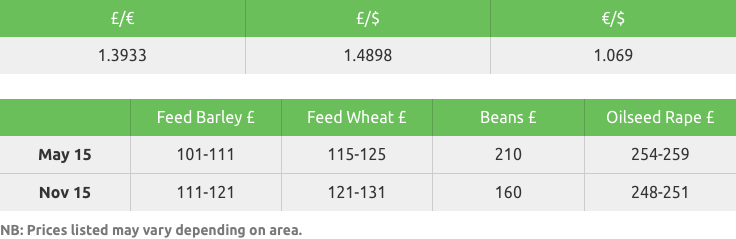

Feed Wheat

US markets have been mixed over the past week, with corn prices pressured by lower oil prices and rising supplies, while wheat firms on continued new crop weather concerns. Continued dryness in the US plains is reported, stressing winter wheat crops with crop ratings deteriorating in key producing states, encouraging fund shorts to trim their positions. US wheat exports remain routine, and with the US$ off multi-year highs coinciding with lower corn prices, the current export projection remains a daunting target. Excessive rains have hampered the very early stages of new crop corn and soy plantings, and if weather problems persist in South America it may support higher prices.

EU prices have firmed €7/t on the week, mainly supported by firmer global markets with the €/US$ up 1c on the week. Another strong week of EU exports, with 1.6mln t of soft wheat licences granted bringing the season-to-date figure to 22.9mln t (21.3mln t at the same time last season), helped to support the market, as cash premiums remain firm against large vessel line-ups. Official reports out of the Ukraine place milling exports at 6.7mln t to the end of February, leaving 400,000t to be shipped in the March-June period –the government has already commented that it will act if the total exported exceeds 7mln t. Russian exports, reported at just over 19mln t to the end of February, have slowed due to the export duty being imposed, and with the uncertainty hanging over the ‘duty’ after 30 June, new crop is almost untradeable, although some was reportedly traded at sub $180 FOB (which equates to £121 sterling) – but on what basis?

The UK market remains similar, with good spot demand against farmers’ reluctance to sell, and with the new tax year a matter of weeks away, a surge in selling is not expected. While this should support spot prices, the ‘snowball’ effect is growing. Official data, at last, placed the UK as a net exporter at the end of January, albeit by 6000t! While the recent rise in UK prices, and sterling, not only almost extinguished the potential of further export trade, it also lowered the import price of EU supplies. Higher than expected imports combined with lower than expected exports leaves the UK balance extremely top-heavy, and unless the UK can erode its stocks, significant price pressure in future months could result.

In summary, it’s been a quiet week. The market is now a battle between bearish old-crop fundamentals and new crop weather/production issues, which may or may not exist. Add in Black sea politics (exports) and you have a potion for a period of increased volatility. One of the most critical period for the market begins in the weeks ahead, as farmers, especially in the US, plant spring crops and winter crops emerge from dormancy. Weather forecasts and planting / crop progress reports will gain in importance, as analysts try and obtain yield potential for 2015/16 crops.

The increased carry-out stocks this season should buffer any reduction in new crop production estimates, allowing total supplies to remain more than sufficient. Talking of politics, it was around this time last year that the Ukrainian/Crimean crisis pushed commodity prices higher, and it may be that the market will need another political crisis of this sort of magnitude to provide the basis for a significant price rally, especially if mother nature behaves herself and delivers what could be another big harvest!

Rapeseed

US soybeans have weakened across the week as the South American harvest progresses and we struggle to find any bullish news. The technical (charts) are looking weak for beans and at present it’s hard to get excited about soybeans.

In the EU we have seen a lack of physical sellers and buyers having to pay high premiums for volume. That said crush margins are very poor and Australian seed will soon be available. We may be seeing a short term squeeze on the futures as the MATIF has ticked slightly higher but it’s hard to see too much upside for old crop futures at this point.

The UK market has eased higher with help from a firmer euro and some crush demand in the spot positions. We have seen some farmer selling of old crop but not in huge volumes. The market remains fairly flat, we feel timing is crucial in this market and it’s not a market to be overly greedy in.

The new crop market is hardly discussed with farmers not coming to the market, we need a story/problem on oilseeds and currently there isn’t one.

Malting Barley

EU new crop malting markets have risen slightly this week on slightly firmer feed barley markets.

UK domestic markets, however, are very quiet with few buyers.

EU spring plantings are progressing very well, on time and into decent seed-beds.

UK sowings are also progressing well and most of the light land in England is now complete. With a good forecast ahead the heavier land should be complete by the end of next week.

Feed Barley

Barley has traded its own market over the past week with values moving marginally higher.

There continues to be a lack of fresh demand in the global marketplace.

Despite this lack of demand, UK feed barley is price competitive and comparably cheap on a FOB basis against other key exporting nations.

Currency volatility continues to put pressure on UK exports, not only for barley. A brief drop in sterling strength was short lived with the release of yesterday’s Budget proving supportive for sterling.

Domestic consumers have shown interest for movement outside of the spot position for the first time in several weeks.

New crop demand remains limited for feed barley for both domestic and export markets.

Oats

The only market change is that spring oat sowing in England started around 10th March on light land and has continued as growers begin to tackle the wetter heavier areas.

Price levels remain static with limited demand now concentrating on May for winter oats and June for all varieties.

Parcels being offered are tonnages over and above existing sales.

The market needs clarity on spring oat planting levels in order to determine the next price direction.

Pulses

The trade is still waiting for a resolution to the currency issue in Egypt, which is holding back fresh sales of old and new crop.

Values for feed and human consumption are coming under pressure as plantings continue apace.

Seed

With spring drillings well underway some growers will be requiring quick top up deliveries. Gleadell can offer several spring barleys and a limited tonnage of spring wheat, as well as Fanfare beans and Daytona peas. However, availability of the most popular varieties is reducing so we would advise growers to cover their requirements.

Autumn 2015 is set to be another good year with many new and exciting varieties being released.

Reflection is a new Group 4 hard from Syngenta and is the highest yielding variety on the 2015 Recommended List. Reflection is earlier maturing than its competitors which could make it a good partner to later maturing varieties. As well as having a very high untreated yield it is suited to light and heavy soils and has a high specific weight. KWS Lili is perfect for big yields and premium potential. Lili is the highest yielding milling variety and is consistent across soil types and regions. KWS Lili is part of KWS’s new ‘Dynamic Wheat’ portfolio, which combines yield and quality.

For conventional oilseed rape growers Campus is a welcome new addition. In 2014 Campus, from KWS, topped many of the trials for gross output amongst the conventional lines. Now newly recommended on the 2015/16 Recommended list it is making its name by being known as “the seed with speed” due to its rapid autumn development. It also has a solid disease portfolio, high gross output and high oil content. For hybrid growers, Incentive remains the variety of choice by many as it has gained farmer confidence. Its high yield potential is made up from seed yield and good oil content.

HOLL (high oleic low linolenic) oilseed rape varieties are available, please contact your farm trader for more details.

Fertiliser

Urea

Interest in urea is building in the UK, with tonnes now being traded at a significant discount to global replacement prices. The weakening of the US $ this week continue to make urea imports into the UK more expensive but with stock already in port side stores importers are now wanting to move product. Urea is available on farm at approximately 61p/kg N compared with imported ammonium nitrate at approximately 76p/kg N and UK AN is priced even higher, so there is certain to be a degree of switching. Spring has not arrived yet and with the current cool temperatures forecast to remain, conditions are ideal to apply urea.

Ammonium nitrate

There are two very separate markets in the UK at the moment with over a £20/t spread between products. GrowHow prices are holding firm as Yara Europe continues to move offer prices higher, while imported prices come under pressure as more product continues to arrive and has to be forced into the market place. Demand is slow as applications are 2 – 3 weeks behind normal so importers have lowered prices in an effort to restart the market, so some very reasonable prices are obtainable for immediate delivery.

Another AN based material on offer is ammonium sulphate (21N + 60So3). Gleadell has two high quality grades available for UK farmers currently. With the need for sulphur being increasingly talked about, grassland users particularly should look at ammonium sulphate this year as a cost effective solution to providing the right amount of nitrogen/sulphur.

NPK/PK

The NPK/PK and straights market has come under pressure this week with blenders competing for tonnes in a quiet market. Typically for this time of year, fertiliser distributers would be at maximum capacity but due to a lack of farmer buying, blenders are struggling to keep prices in line with replacement costs of raw materials. Despite a rise in both phosphate and potash, on farm levels have dipped again which has encouraged some uptake. Haulage is still a problem in the UK and although we are past the worst of the logistical problems, farmers should bear in mind that most suppliers will be unable to deliver immediately on receiving an order. Blenders have now moved to April deliveries so we urge any buyers to order as soon as possible. Gleadell offers excellent finance options to spread the cost of fertiliser. For more information please contact your local Gleadell Farm Trader.