| 2015-02-20 |

The recent bout of heavy rainfall and further showers forecast across the UK has delayed first fertiliser applications. Importers are using this time to discharge delayed vessels and move tonnes swiftly through bagging to catch up with deliveries.

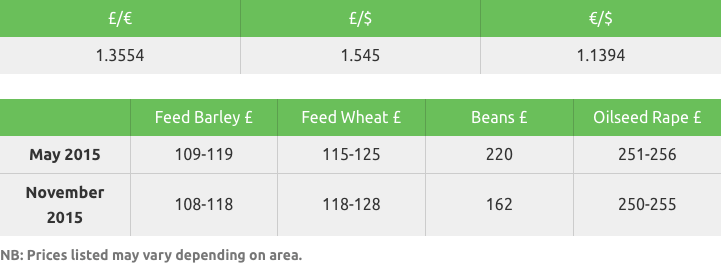

Feed Wheat

With an increased threat of colder weather entering the US Midwest, markets found support into the long weekend, which continued into early this week before trading lower. Reports that the USDA Agricultural Outlook Forum may predict a lower-than-expected US wheat area for the 2015/16 season also supported, although analysts still believe that US 2014/15 wheat stocks will increase further due to US exports being uncompetitive. This was confirmed, with Egypt tendering (after receiving confirmation that further Russian exports would not be exempt from the current export duty) for US wheat in a tender using the $100mln credit line, only to cancel the tender due to the offered prices being too high.

EU prices, initially supported by the move higher in the US, have eased back in recent days as the realisation of ample stocks starts to weigh on sentiment. Despite the continued strong export pace (now including French feed wheat sales to Asia), and officials estimating soft wheat exports for the season exceeding last season’s record, stocks are still projected to rise year on year. Russian exports have all but stopped since the export duty was imposed on 1 February. They are currently reported at 18.56mln t, with 1mln t still to be shipped on deals concluded prior to the duty being imposed. News that the Russian government will review the current duty when February’s exports are known throws more confusion into the market. Traders try to second guess whether this means a possible extension of the duty if exports are too high, or a reduction or removal of the duty if the government feels comfortable with stocks levels and are more optimistic over new crop prospects.

UK values again followed global markets higher, only to fall in line with the other exchanges. Lower inflation and unemployment figures have boosted sterling in the past days, and apart from existing export business being executed over the next few weeks, the UK remains uncompetitive for further intra-EU trade. Asian big-vessel feed interest continues to surface once in a while, although cheaper corn prices and impending sub-Asian harvests are seen limiting demand. UK market logistics are still governed by a general lack of producer selling, but with domestic usage and further exports trade far from robust, the UK still faces the likelihood of an above-average carryout of stocks at the end of the season. News that one of the UK wheat-based ethanol plants is broken (yet again) and the other is undergoing prolonged maintenance only adds to the prospect of ending this season with record carryover stocks of wheat .

Milling premiums have eased back by a few pounds recently, pressured by low flour volumes and by a keenness to secure homes for wheat in the next month or so.

In summary, weather remains a key factor that could support the market at present. The weather is far from ideal in the US and parts of the Black Sea region, with recent cold spells putting new crop plantings under stress. Until crops have emerged from dormancy and better yield assessments can be obtained, weather scares will keep markets nervous. There is no shortage of old crop supplies available and unless next season’s potential supply issues are confirmed into actual major crop losses, market rallies will remain limited and provide selling opportunities. The outlook forum may provide short-term support if the numbers are lower than trade expectations, but with the US uncompetitive even with a sole origin credit line, further increases in stocks may offset the lower planted area.

Rapeseed

Rapeseed prices remain capped by an extremely strong pound / euro exchange rate but are supported by reasonably good demand for physical seed and by an extremely volatile, but mainly firmer, soy market. Farmer old crop long holders are gambling that the fundamentals of the rapeseed market (which are bearish) turn around fast enough to enable a market rally before new crop arrives .

Malting Barley

Old crop markets are few and far between as we progress towards the end of the season with maltsters across the EU remaining well-stocked and absent from the market.

Malting barley prices have weakened, following the wider grain market. further pressurised by the firmer pound/weaker euro and resultant weaker FOB values.

Australian malting barley exports destined for China have slowed as demand is nearly fulfilled.

Interest in new crop malting barley has grown on the back of the estimated increase in spring area for the UK and EU. However an absence of sellers has slightly supported EU prices.

Good premiums for new crop malting barley continue; we recommend contracting a proportion of new crop tonnage sooner rather than later.

Gleadell has contracts available for the new high yielding spring varieties RAGT Planet and Limagrain’s Octavia.

Feed Barley

Reduced demand into both export and domestic homes has led barley values to drift lower over the past week.

The driving factor for UK barley exports this season has been the knock on impact of strong French exports to China, creating increased opportunities into both North African and Asia.

China is celebrating its New Year holiday and will be until at least 24 February, removing a key driving factor from the barley market.

Domestic consumers have been in the market, albeit for small top-up tonnages.

FranceAgrimer revised its barley ending stock figure upwards yesterday to 1.74mln t, some 250,000t higher than last month.

Oats

An extremely quiet market as limited demand now pushes forward to May/June with few offers appearing as long holders wait for better days.

Uncertainty remains as to the level of spring oat plantings, which have yet to start.

Pulses

Old crop demand has disappeared as cargos arrive replenishing stock for Ramadan. Further interest is being discounted and positions are unlikely to appear until April/May at the earliest.

New crop remains very quiet with feed values unchanged at £30/t over LIFFE wheat plus upgrades.

Seed

Spring seed demand has been high this week. Most spring barley varieties are available, including Propino, Concerto and Odyssey, as well as new variety KWS Irina and two further newcomers requiring acreage for evaluation malting contracts – RGT Planet and Octavia.

Spring wheat is now extremely limited although spring oats are in good supply. A limited amount of pulse seed remains available for growers looking at EFA requirements or three-cropping requirements, including spring beans Vertigo and Fanfare and the large blue pea Daytona.

Looking ahead to the autumn Gleadell can offer attractive terms on Campus, a new conventional winter oilseed rape variety from KWS. Campus has been added to the 2015/16 Recommended List after a fantastic year in 2014, topping many of the trials for gross output amongst the conventional lines. Branded “the seed with speed” due to its rapid autumn development. Campus is a great all round package with high oil content, high gross output and a solid disease portfolio. Campus is available with deferred payment, please speak to your Gleadell Farm Trader for more details.

Other new varieties featuring within the new season portfolio including Wembley, top of the candidate list, SY-Harnas, a high yielding variety with good LLS resistance, and DK Exalte, a superb all-round variety with solid disease ratings and high gross output. Farmers’ favourite Incentive and the TuYV resistance conventional Amalie are also available.

Fertiliser

The recent bout of heavy rainfall and further showers forecast across the UK has delayed first fertiliser applications. Importers are using this time to discharge delayed vessels and move tonnes swiftly through bagging to catch up with deliveries. All blenders have now moved onto March deliveries and with many growers still to order final requirements, we urge that tonnages are booked immediately to avoid late or non-delivery.

Urea

Global urea markets remain weak for spot shipments with little fresh demand. European and US markets remain flat, although traders anticipate market activity picking up in the coming weeks. In the UK, demand remains low. However, we expect the next flurry of purchases over the next couple of weeks.

Ammonium nitrate

This week UK producer GrowHow increased its February terms by £3/t. Levels for March delivery on both UK and imported product are up by £5/t so buying sooner rather later is recommended.

NPK/PK

As mentioned in last week’s report, phosphate prices continue to firm with significant buying from India and Europe. However in the UK phosphate for straights continues to be squeezed as blenders and merchants compete for spring tonnes. Blended NPK/0PK products are up on last week and will continue to firm in the weeks ahead as demand increases. For more information on available grades and delivery windows, please contact your local Gleadell Farm Trader.