| 2013-12-20 |

The UK wheat market remains a ‘follower’ of other markets but has only lost £1 over the week. Reported imports for October were higher than expected at 221,190mt, bringing the season-to-date total to just over 1.05mln t.

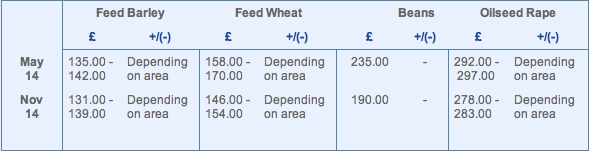

Feed Wheat

US markets continue to fall under pressure from routine wheat sales/export inspections and growing concerns over corn exports to China. With the US concentrating on shipping its huge stockpiles of corn and soybeans, wheat exports have been placed on the ‘back-burner’ leading many to question whether seasonal sales will match the current US projection. Reports claim that China has now rejected 10 cargoes (600,000t) of corn, leaving US shippers scrambling to switch ‘on-sea’ shipments at a financial loss, again leaving a question mark over the long-term shipping program to China, and the recently inflated export projection.

The EU ‘cash’ market, although not successful in the recent Egyptian tender, remains firm in the spot position based on the strong current export pace. French prices had a hefty $10 premium build-into their latest Egypt price, and this time Egypt refused to pay the premium! Exports are now reported for the season at 13.3mln t (a rise of 40% year-on-year) and the fact that Egypt paid an inflated price over its previous purchase in a market (CBOT) that had declined $15/t illustrates the current ‘cash market squeeze’.

The UK market remains a ‘follower’ of other markets but has only lost £1 over the week. Reported imports for October were higher than expected at 221,190mt, bringing the season-to-date total to just over 1.05mln t.

In summary, the spot cash markets are , for the moment , behaving differently from the bearish fundamental futures markets. It’s all currently down to who wants the wheat, and from where can one source it! With the festive period now upon us, farmers have shut–up shop, transport remains a pivotal problem and supplies will be hard to source until January . When the trade gets ‘up and running’ and the apparent spot tightness loses its grip the overall bearish fundamentals may paint a different picture for markets . We need a weather problem to spark a rally in prices .

Oilseed Rape

Autumn drilling is now finished in many areas. Growers are now focussing on spring cropping requirements.

Spring barley has been in strong demand, particularly Null-lox. We have a limited amount of Cheerio available with other varieties now sold out.

Demand has also come to conventional varieties including Propino/Odyssey/Concerto and the new variety Sanette.

Moving to spring wheat there has been interest in the quality wheat Mulika and Dafne and the feed variety KWS Alderon.

Spring peas still offer the grower the strongest gross margin available from a spring crop along with perfect entry for 1st wheat.

The large blue Daytona and Marrowfat Kabuki have been of interest to growers along with very attractive buyback contracts.

Looking ahead to autumn 2014 - Gleadell have launched the first variety of the OSR portfolio, the new addition to the top of the RL list Incentive from breeder DSV, which combines consistent seed yield with outstanding oil content to offer the grower a solid variety to fit into the farming system. We have an early order offer with early delivery and delayed payment.

Malting and Feed Barley

There is continued demand for low nitrogen spring varieties including Tipple and Propino as well as for winter varieties, namely SY Venture and Cassata.

Malting premiums have benefited from a lack of export demand for UK feed barley, however with feed prices set to track lower in the new year, growers should look to market their malting barley as markets become available to make the most of current premiums.

Malting export values have remained unchanged over the past week as there is a continued lack of demand for old crop and new crop interest remains steady.

The latest North African barley tender saw UK feed barley lose out to Argentinian supplies again . The price difference was $14 pt (£9 pt ) . Sooner or later the UK surplus will have to come to market and there is no shortage of other origins – France , The Black Sea and Argentina to name three .

Gleadell still have a variety of 2014 contract options available including Null-Lox for January/March and April/June positions as well as conventional springs throughout the season.

We have distilling contracts available for Concerto and Odyssey on both premium over wheat futures and non defaultable pool.

Gleadell are pleased to still be accepting tonnage into our pool’s for crop ’14. These are available for conventional springs, Tipple and Propino, as well as winter varieties SY Venture and Cassata.

Oats

The mild weather has prevented the usual seasonal lift in demand from the supermarket shelves for oat products.

There is a small demand from the ports for feed oats, but this price has to compete with the compounder who is a keen buyer with the current attractive discount to wheat.

Autumn plantings of oats went into good seed beds and this acreage is expected to be back to levels previously seen in 2011 which should start to return the market closer to equilibrium.

Seed

Autumn drilling is now finished in many areas. Growers are now focussing on spring cropping requirements.

Spring barley has been in strong demand, particularly Null-lox. We have a limited amount of Cheerio available with other varieties now sold out.

Demand has also come to conventional varieties including Propino/Odyssey/Concerto and the new variety Sanette.

Moving to spring wheat there has been interest in the quality wheat Mulika and Dafne and the feed variety KWS Alderon.

Spring peas still offer the grower the strongest gross margin available from a spring crop along with perfect entry for 1st wheat.

The large blue Daytona and Marrowfat Kabuki have been of interest to growers along with very attractive buyback contracts.

Looking ahead to autumn 2014 - Gleadell have launched the first variety of the OSR portfolio, the new addition to the top of the RL list Incentive from breeder DSV, which combines consistent seed yield with outstanding oil content to offer the grower a solid variety to fit into the farming system. We have an early order offer with early delivery and delayed payment.

Fertiliser

Urea

The increases in international values seen over the last two weeks are holding firm, short covering of sales already made is maintaining those values. Algeria are still unable to supply product, leading to further short covering from traders. India are still buyers of urea, with a tender expected shortly. Supply to India would be expected from China or the middle east, adding to further bullish news. As the UK market slows down for Christmas, many other countries have no such holiday. The firmer feel to the market is expected to continue. Current replacement values for granular urea today are around £315 tonne on farm UK.

AN

As we enter the northern hemisphere’s peak usage season for AN and CAN, demand from domestic consumers in Ukraine, Lithuania, Russia, France and Germany is keeping product supply tight. Domestic demand is these countries is taking precedence over export to the UK and further afield. Overall in the UK this is driving values firmer. Between now and early in the new year, increases of around £10-£15/t are expected for imported product. UK produced ammonium nitrate is in the market place at levels competitive with imported product with deliveries currently available for January to March.

Sulphur

With delays to the import schedule for imported NS grades early in the fertiliser season, and increased sulphur demand overall, supply is getting tight for some sulphur products. We still have available GrowHow nitrogen sulphur grades, with production moving on NPKS products, it’s only while stocks last.

SKW Piesteritz

For spring delivery we have available both Piamon, 33N 30so3 and Alzon 46% stabilised nitrogen product. Between these two products we have a proven fertiliser system that provides excellent efficiency and yield increases over a traditional fertiliser system. Piamon on its own is a highly competitive compound NS grade, for spreading up to 36M. With product available for Jan/Feb, many orders have appeared this week.

P & K

In a similar way to nitrogen fertiliser, the domestic UK market is much firmer with buying activity, for Jan – Feb delivery. The expectation for PK and NPK blended products is a £10-£15 increase coming from 1st January onwards.

After a busy week for straight phosphate and potash demand, values are buoyant.

Internationally potash is stable to firm with trade continuing at expected values, spring demand will drive this up further. This week the phosphate market has seen a jump in US domestic market values with further demand from China, South America and Australia evident . In the UK market, a rise of £15-£20 pt would be expected as stock is run down and replacement values filter through.